April 2014 Newsletter | Leinonen Lithuania

|

|

|

Dear reader,

Leinonen Lithuania has established an advisory unit. Besides assisting clients in company establishment and liquidation processes, consulting on labour issues, advising on tax and accounting policies, communicating with tax authorities on behalf of the client, providing tax and human resource compliance services, this unit provides summary of tax, accounting and legislation news to clients and other interested parties.

Please find below the main changes that were introduced during first quarter of 2014

|

|

Tax, accounting, and legistlation changes

|

|

40th Business Accounting Standard “Introduction of the Euro”

|

|

|

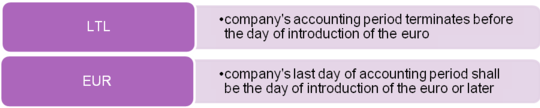

Lithuania is willing to become the member of the eurozone from 1 January 2015. On 28 March 2014 the 40th Business Accounting Standard “Introduction of the Euro” was approved, which defines the major requirements to the companies that apply business accounting standards:

- 1.Requirement for the recalculation of accounting data, expressed in litas, into euro

- 2.Drafting of financial reports and recalculation of comparative information, expressed in litas, into euro, as well as the provision of additional information in the explanatory note

- 3.Account keeping over the period of cash turnover in euro and litas

- 4.Accounting of costs associated with the introduction of the euro

Currency of financial accounts:

|

|

Amendment of Article 30 of the Law on Corporate Income Tax relates to the carrying forward of tax-related losses

|

|

|

From 1 January 2014 a new provision on corporate income tax related to the carrying forward of tax-related losses came into force. Tax-related losses shall be carried forward for an unlimited period, however, the amount to be carried forward shall not exceed 70 % of the taxable profit. Therefore, a company that makes taxable profit in 2014 will be obliged to pay at least 30 % of calculated corporate income tax for the fiscal period in 2015.

|

|

Amendment of the comment on the corporate income tax related to the attribution of surplus or shortage of goods, determined during inventory, to allowable deductions

|

|

|

During the stock inventory the surplus or shortage of some goods may be identified quite frequently. The possibility to re-sort the goods only after the approval to attribute the shortage of quantity of goods, obtained after re-sorting, to not allowable deductions depends on whether the goods are homogeneous or not.

Attribution of goods to homogeneous or not must be justified in the internal procedures of the company. Any goods shall be considered homogeneous when the goods have analogous consumption purpose, appearance, composition, quality and the price of which is identical or differs slightly.

Only homogeneous goods may be subject to re-sorting. Provided that during the company’s inventory the surplus of one kind and shortage of other kind of homogeneous goods is determined and after re-sorting of goods the shortage of quantity is identified, such shortage shall be considered as not allowable deductions according to Article 17 paragraph 1 of the Law on Corporate Income Tax. The shortage of value, determined after the re-sorting of homogeneous goods during the company inventory, shall be considered allowable deductions, whereas the surplus value shall be attributed to taxable income.

Upon the determination of surplus of homogeneous goods after re-sorting, it is included into taxable income, i.e. taxable profit is increased by the sum of surplus goods determined during inventory. Once the homogeneous goods are sold, such surplus sum (sum of purchase prices of homogeneous goods) shall be included to the allowable deductions.

|

|

Information on the status of employees’ safety and the conformity of workplaces to the legislative requirements

|

|

|

Under the order of chief inspector of the State Labour Inspectorate under the Ministry of Social Security and Labour of the Republic of Lithuania it is permitted to not provide information to the State Labour Inspectorate on the status of employees’ safety and the conformity of workplaces to the legislative requirements of occupational safety and health when only one employee is employed in the company.

This order comes into force from 1 April 2014.

|

|

Provision of data on shareholders to the Centre of Registers

|

|

|

From 1 January 2014 amendments of the Law on Companies of the Republic of Lithuania have come into force defining that it is not necessary to make a list of shareholders when the shareholder of the private limited liability company is one person. When the private limited liability company has more than one shareholder, a list of shareholders must be drawn up, but the provision of such list to the registrar of the Register of Legal Entities is not required anymore. Information on shareholders is provided by means of a new system directly to the registrar of the Information system on the partners of legal entities within 5 days from the registration of the private limited liability company at the Register of Legal Entities.

The new data system is not functioning yet, though the provision of data has been planned to be launched from 1 January 2014. Once the system starts functioning, all the private limited liability companies, including the ones founded before 1 January 2014 or having more than one shareholder, will be obliged to provide data on their shareholders.

Up to date any information on the shareholders of private limited liability companies was stored in scanned documents only.

|

|

Bilateral agreements of the Republic of Lithuania on the avoidance of double taxation

|

|

|

From 1 January 2014 the application of the agreement between the Government of the Republic of Lithuania and the Government of the Republic of Kyrgyz on the avoidance of double taxation and prevention of tax evasion has been started.

Currently, 50 agreements on the avoidance of double taxation are being applied in Lithuania.

|

|

Do you need advise in Lithuania?

|

|

|

Leinonen Lithuania helps companies enter and succeed in the Baltic and Lithuanian markets.

If you need any help or more detailed information, please contact:

MAŽENA BIRBALIENĖ

Head of advisory unit

tel. +370 5 237 504 0

e-mail: mazena.birbaliene@leinonen.lt

|

|

|

Note: The newsletter is just for information purposes and doesn’t constitute a legal opinion or professional advice.

|

|

Follow Leinonen Group in Social Media

|

|

|

Leinonen Group is a Finnish-owned private accounting and advisory company, which was established already in 1989. Leinonen Group helps companies enter and succeed in challenging business environments by offering reliable accounting, payroll management, advisory, administration, and audit services. The deep local expertise and personal service approach, combined with wide international presence, is our strength. Our 13 offices can be found in the main cities of 11 countries – Finland, Sweden, Norway, Estonia, Latvia, Lithuania, Poland, Bulgaria, Hungary, Russia, and Ukraine.

Read more: www.leinonen.eu

|

|

|

Leinonen Lithuania

Vilnius | Kaunas

+ 370 5237 5040

leinonen@leinonen.lt

www.leinonen.lt

|

|

|

|